The Optimisation Trap

Why RGM is the engine, but Category must set the direction

A Buyer’s Lens perspective

Most commercial strategies look robust on a slide deck.

Far fewer survive contact with reality.

That gap - between internal logic and what actually lands at shelf, in negotiations, and inside retailer decision systems - is why The Buyer’s Lens exists.

I’ve spent over 25 years inside FMCG commercial organisations: first as a retail Buyer, then in supplier-side Category leadership roles, and more recently advising senior teams navigating a growth environment that has become structurally tougher.

Across those roles, one pattern has become increasingly clear:

Organisations have more data, more tools, and more analytical power than ever before - yet confidence about where to grow, what to prioritise, and which trade-offs truly matter has rarely felt lower.

This tension sits at the intersection of two disciplines that already exist in most businesses: Category and Revenue Growth Management (RGM).

Why this matters now

In a low-growth, margin-pressured environment, influence has in many cases shifted decisively towards RGM.

That shift is rational.

It is financially driven.

And in many ways, it has been overdue.

RGM brings discipline to pricing, promotion, mix and investment decisions. It speaks the language of CFOs and Boards. It offers measurable levers, scalable governance, and short-term control in an uncertain world.

None of this is wrong.

But control, on its own, is not the same as direction.

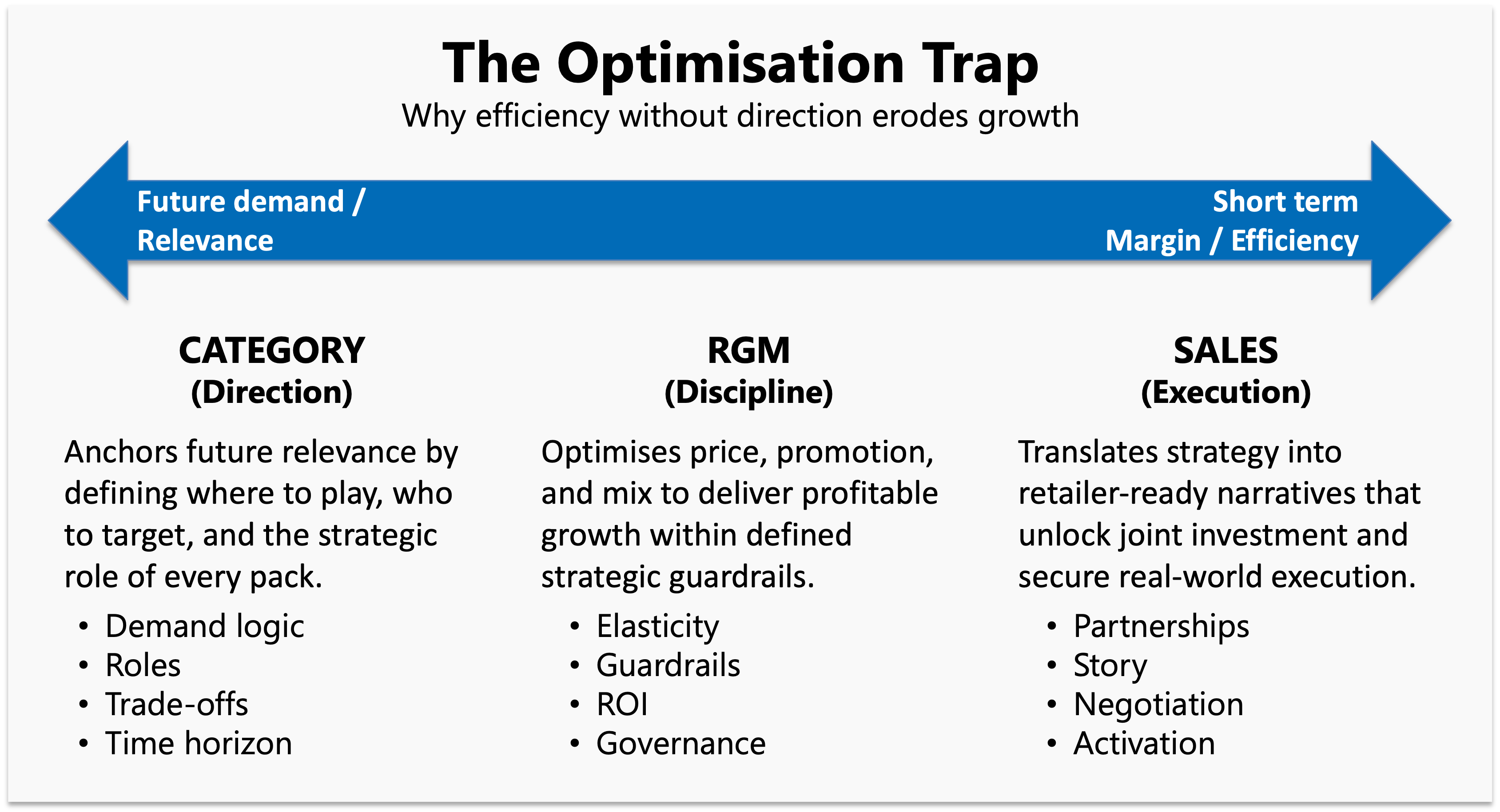

The Optimisation Trap

The Optimisation Trap

When optimisation leads without shared direction, organisations can become highly efficient at managing portfolios whose relevance can quietly erode.

Sustainable growth requires direction, discipline and execution - designed and governed as a single commercial system.

What the research is already telling us

Over the past few months, I’ve been running a research programme on the future of Category and commercial decision-making, combining quantitative survey data with in-depth interviews across senior Category, Sales, RGM and Retail leaders.

When examining the barriers to Category performance, two signals stand out clearly:

64% cite organisational silos

67% cite weak retailer–supplier collaboration or misaligned incentives

These are not separate problems.

They are two sides of the same issue.

When internal teams show up to retailers with fragmented logic - Category telling one story, RGM (or the actual proposal) another - collaboration weakens, trust erodes, and even well-intentioned optimisation starts to feel supplier-centric rather than shopper-led.

The issue is not a lack of disciplines.

It is how those disciplines are separated, prioritised, and presented to the outside world.

Why RGM rose — and where the limits appear

RGM addresses some of the most acute boardroom questions:

How do we reduce margin leakage?

How do we create consistency across markets?

How do we improve the return on trade and promotion?

At its best, modern RGM does far more than tweak price points. It integrates elasticity, pack architecture, value tiers and promotional response into a disciplined commercial system.

But even the strongest RGM frameworks are anchored in current and historic demand patterns.

They are less well equipped to answer a different, more fundamental question:

Where should future demand come from? And which roles, shoppers and trade-offs matter most over the next three to five years?

That question sits squarely in Category’s remit.

Where optimisation breaks down

The challenge is not that RGM exists.

It’s that RGM and Category too often operate in parallel rather than in partnership.

In many organisations:

Category teams generate insight that can stop short of hard trade-offs

RGM teams optimise price, promotion and mix without a fully shared demand logic

Sales and Marketing sit in the middle, arbitrating between the two

Everyone is working hard, but not always from the same starting point or the same end objective.

RGM can tell you the optimal price for a declining brand.

What it cannot do on its own is answer:

Is this the right category, portfolio or role to be optimising in the first place?

This is how organisations fall into the Optimisation Trap: becoming highly efficient at managing portfolios whose relevance is quietly eroding.

Relevance risk vs margin risk

Finance teams understandably focus on margin risk.

But there is another risk that is harder to see on a spreadsheet: relevance risk.

It eventually shows up as:

Penetration drift as recruitment packs are priced out

Base volume erosion as shoppers reframe the category

Mix degradation as promotions over-reward low-value segments

Weakening pricing power as brands lose distinctiveness

RGM manages the financial P&L.

Category, when done well, manages the relevance P&L.

Sustainable performance requires both.

Integration, not substitution

This is not a choice between Category and RGM.

When integration works well:

Category sets direction: where to play and why

RGM governs discipline: how value is monetised

Sales executes credibly: translating strategy into retailer-ready narratives

Category does not replace RGM.

It ensures optimisation is applied to the right strategic choices.

Closing thought

The companies that win in the next decade won’t be those with the best algorithms. Those are becoming table stakes.

They will be the ones that can distinguish between a profitable transaction and a profitable relationship - and design commercial systems that protect both.

RGM remains an essential engine.

But engines need direction.

Where this goes next

In future editions of The Buyer’s Lens, I’ll explore:

What modern, decision-led Category capability really looks like

Early synthesis from the research programme

How organisations redesign decision rights, roles and governance for tougher growth environments

If this resonates, you can find more of our thinking and research at optimaretail.com - or follow along here.